Reporting to stakeholders

ERICs report to a wide range of stakeholders with whom the ERICs interact and who have differing needs for accountability. Although the Members States are seen as the primary users of ERICs activities and financial information, the stakeholder list is much wider and includes:

- The European Commission

- The Host Organisation

- Employees

- Other European Research Institutions

- Partner Organisations

- Regulators

- Other investors

- Suppliers

The stakeholders’ accountability needs have to be fully understood and the overall information provided by the ERICs should address these needs. Whilst recognizing that the ERICs performance is important, the purpose of accountability is to make sure that the ERICs managers act in a relationship with the providers of funds. The relationship should be based on trust, shared collective goals and relational reciprocity.

Users of ERICs accounts – primarily the Assembly members – need to make decisions about future resources and to assess the accountability of the management. Financial reporting is there to provide them information that allows them to assess whether:

- The current levels of charges are sufficient to maintain the volume and quality of services provided and the accomplishment of the statutory goals

- The ERIC is achieving the objectives established as the justification for the resources raised during the reporting period

- The ERIC is using resources economically, efficiently, effectively and whether such use is in their interest: users are likely to make decisions about more than economic resources, but also social and scientific impact aims.

Narrative reporting

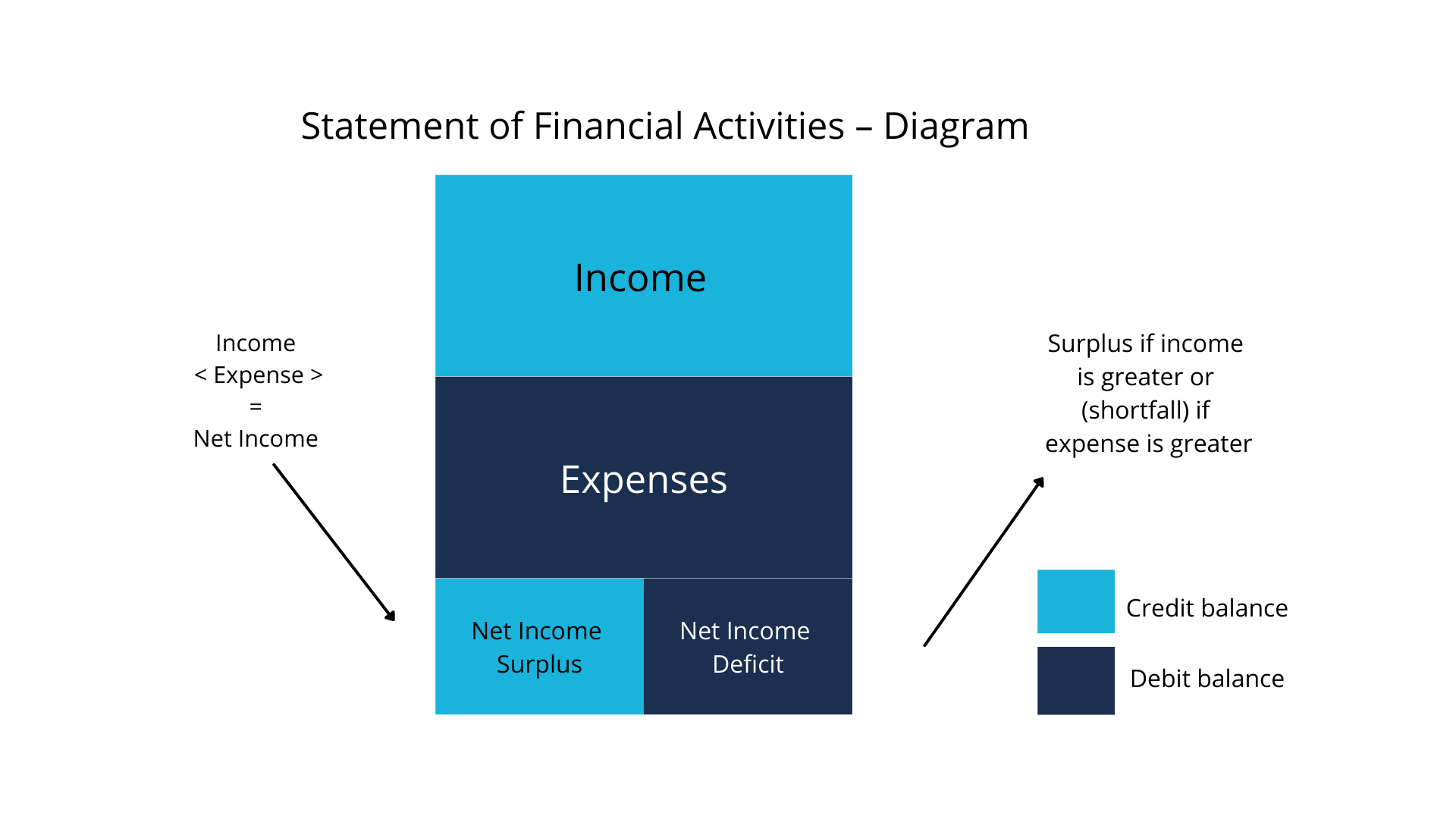

Terms such as profit, and loss, which permeate the business accounting standards, are not suitable for ERICs. In particular, the concentration indicator of performance confuses the meaning behind ERICs financial reporting which should be focused on the European Research and development cohesion objectives. Therefore, narrative reporting is absolutely essential in ERICs reporting.

Narrative reporting describes the non-financial information included in annual reports to provide a broad and meaningful picture of activities, performance, impact and future prospects. This includes the strategic areas/services being developed, the directors’ report, the chairman’s statement, the directors’ remuneration report and corporate governance disclosures. Income statement descriptive Report should include relevant non-financial information. In fact, appropriate and detailed non-financial information can add significant benefits to the ERICs in terms of engagement and reputation. In fact, the practice of disclosing and being accountable to internal and external stakeholders, reporting on financial, environmental and social performance enables the ERICs to be transparent in communicating these non- financial aspects of their management and performance.

Non-financial information for ERICs is as important as financial information in the decision-making process: both pieces of information contain valuable insights to make a decision, evaluating potential alternatives, choosing the best option based on existing alternatives, monitoring implementation strategies and checking progress periodically. s.

Though many ERICS produce a variety of versions of this report calling it various names such as budget report, profit & loss, income and expense – shows the ERICs income and expenses for a specific period of time. The statement reflects the changes to ERICS’ net assets resulting from income and expenses that occur during the current fiscal year.

TIP

See examples of narrative reporting styles in annual reports below.

Mandatory auditing process

An independent audit is an examination of the accounting records and financial statements by an independent auditor—normally, a certified professional accountant (CPA). The auditor carries out an independent analysis to test the accuracy of the accounting records and internal controls. At the conclusion of the audit, the auditor issues a report in the form of a letter stating whether, in the auditor’s professional judgment, the examined accounting records and year-end financial statements are fairly represented according to generally accepted accounting principles (GAAP) or to the IFRS . The auditor’s letter should be attached to the front of the financial statements.

All ERICs are required to obtain audits, to obtain what is termed a “single audit” to test for compliance with European grants management standards. In addition, Member States require ERICs to be audited if they solicit funds and will not provide funding unless they receive audited financial statements. This is confirmed by the COUNCIL REGULATION No 723/20099 whereas in art. 13 (Budgetary principles, accounts and audit)it is stated that “an ERIC shall be subject to the requirements of the applicable law as regards preparation, filing, auditing and publication of accounts”.

Figure 1: Comparison of Common key factors and differences in financial reporting

The results of the year’s activities result in a change to the ERICs net assets. Net results (Cash-carry over) for each year are accumulated and show as changes – increases or decreases – in those net assets categories. Net assets beginning balances in each expense category are increased by each year’s surplus and decreased by each year’s deficit. However, it should be highlighted that some ERICS (eg ESS ERIC) do not generate a surplus according to their accounting policy.

A well-formatted reporting provides accurate and relevant information with enough context for the board to thoroughly understand what’s going on with your organization financially. To be strategically useful, the reports should show numbers in context so a ERIC Assembly Members could answer the following questions:

- What was the total revenue/expenses of last year?

- What is the annual budget for this year and what are the variances with respect to the budget?

- How do we expect to end the year and how does that compare to the approved budget? What are the reasons for the significant variances?

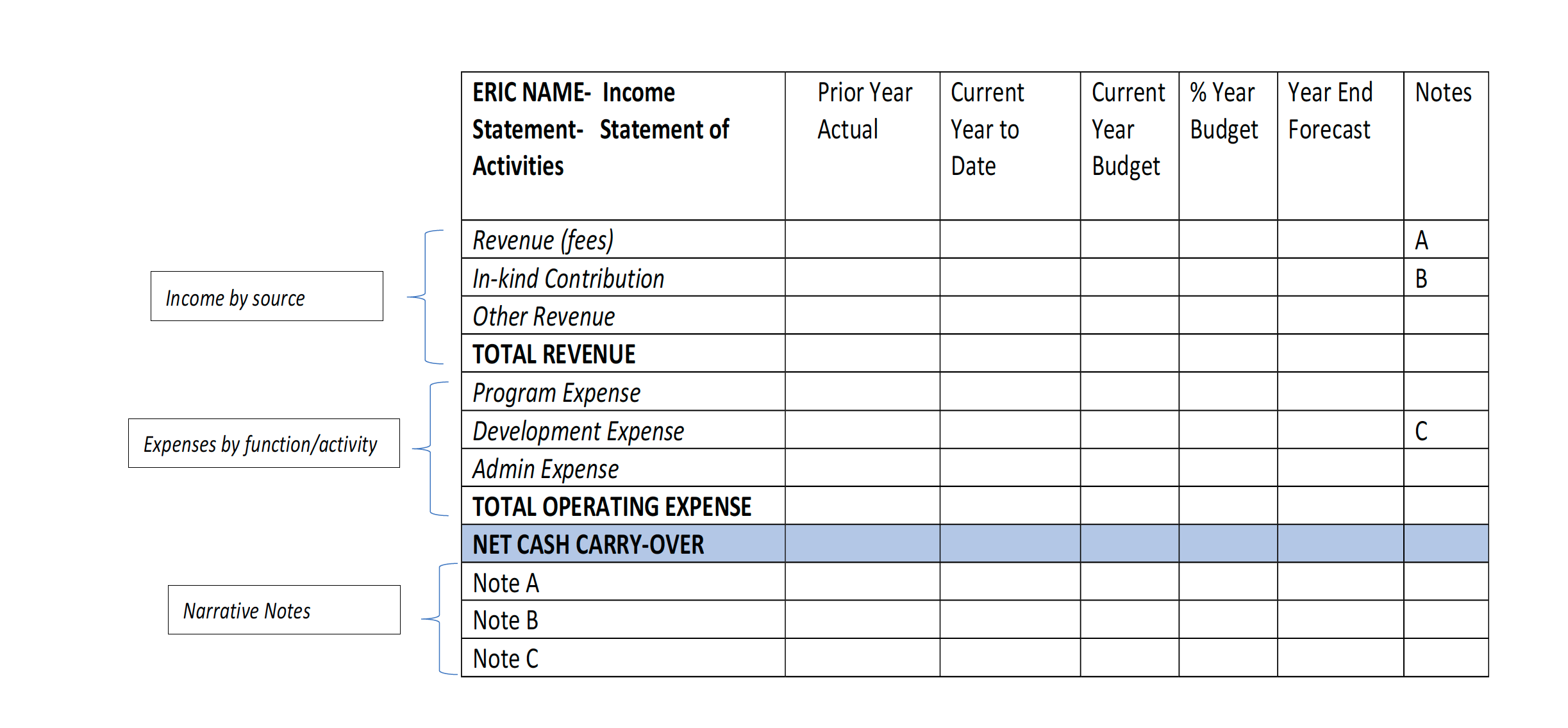

Below (Figure 2) is a general format for an Income Statement recommended for ERICS’ internal reporting purposes. The report for an ERIC should include detailed line items in each category, but the objective would be to keep the report at one page in length, although narrative explanations may flow to a second page.

In this report design, income is shown by source (membership fees, in-kind contributions, R&D Projects) and subtotaled separately as earned and contributed. Within earned and contributed categories, you may include additional line items to show more detail such as earned income by program, or each contributed income by source such as member Countries, and special events.

Expenses can be shown as aggregate figure or by major program activity. Showing expenses by activity (function) clearly demonstrates how the ERIC spends its resources toward accomplishing mission activities.

The prior-year total provides context for comparison. The annual budget as approved by the Assembly is shown as well as a year-end forecast in lieu of frequent budget revisions. The forecast column is equal to the budget column at the beginning of the year to reflect anticipated changes from the original budget. Variances between the approved budget and the year-end forecast are to be shown both in Euro amounts and in percentages, and significant variances should be noted and explained.

The major source of revenues are the “Membership fees”. The item “Other revenue” item may include the EC grants and the funding provided by other third parties.

Figure 2 Internal report format

The report format (Figure 2) is designed to promote maximum understanding by the Assembly of Members Countries by showing the year-to-date but focusing on the expected year-end results. Management updates the year-end forecast to reflect expected changes to line items, focusing on what can be done to mitigate changes that might cause a deficit.